The Wall Street Journal Guide to Student Loans

This guide aims to dispel some of the misconceptions about paying for college, taking on student debt and what graduates earn. The Journal has analyzed a vast trove of federal education data to more definitively say which schools offer a good financial return and which leave graduates with crippling loans.

Click Here to Review the Information Online

Some Highlights from WSJ Guide

What is the Difference Between "Financial Aid" and 'Scholarships and Grants'?

- Scholarships and grants are awards that students don’t need to repay. Schools may give them because of financial need, or to reward high grades, athletic ability or other talents. The federal government gives Pell grants, generally benefiting low-income students.

- Financial aid is more of an umbrella term that includes scholarships and any other monetary assistance students receive to cover school costs, including campus jobs through a federal work-study program and student loans. (Page 13)

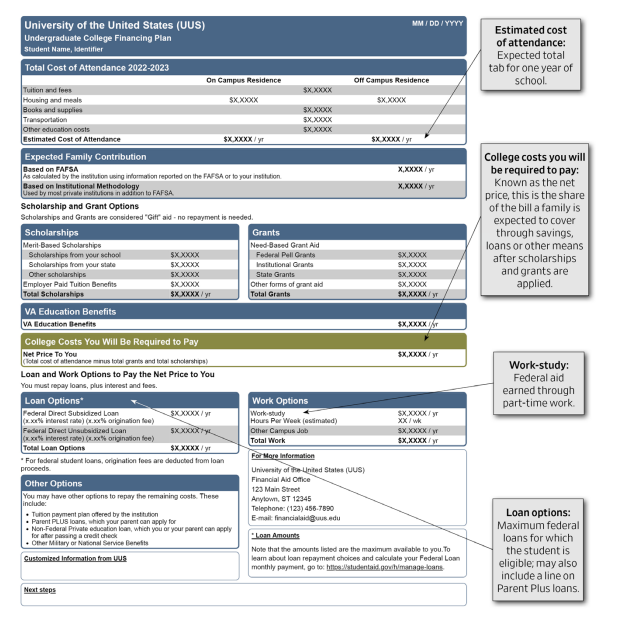

Sample "College Financing Plan" (Page 15)

DecidED: A Free College Cost Comparison Tool

DecidED helps students quickly and accurately understand the affordability of their college options without needing to do financial aid interpretation alone. Advisors and administrators use DecidED to track and support student progress on their college journey.

Our free college cost comparison tool gives students, advisors and partner organizations an easy way to understand college costs and other fit factors.

Click Here for more information.

Our free college cost comparison tool gives students, advisors and partner organizations an easy way to understand college costs and other fit factors.

Click Here for more information.

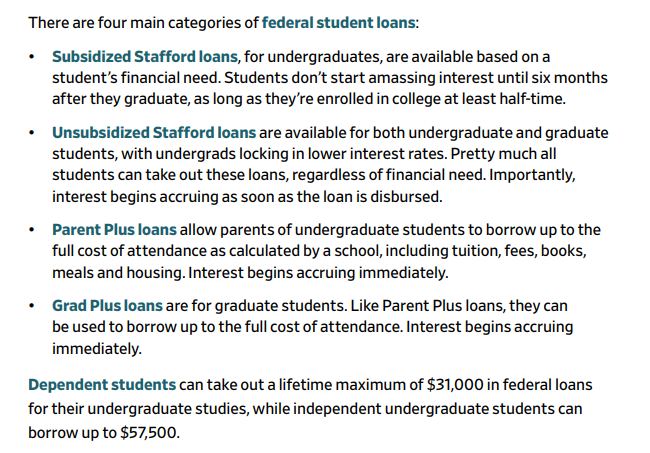

What are the types of federal student loans, and how do I get them? (Page 18)

- Students don’t need to pass any sort of credit check to qualify for loans, and parents will get the all-clear as long as they don’t have an adverse credit history, like having declared bankruptcy (see Chapter 3 for more on parent loans).

- People who aren’t U.S. citizens may have limited access to federal aid but qualify for state and institutional funding.

- Veterans and families of military members may qualify for separate education benefits.

- Borrowers also can be rejected for federal student loans if they have previously defaulted on a federal student loan or if they fail to maintain satisfactory academic progress.

What are the steps to receive student loans? (Page 19-20)

- Fill out the Free Application for Federal Student Aid, or Fafsa, available on the Federal Student Aid website beginning on Oct. 1 of each year, for aid to be used the following school year. Applicants can use an IRS tool to pull information from their tax filings, easing the process a bit. Have handy any recent bank statements and investment account balances as well. For those applying to undergraduate and many graduate programs at nearly 300 schools, most of them private, also complete the College Board’s CSS Profile. That’s short for College Scholarship Service (see Chapter 2 for more details on this form).

- Be prepared to wait. The school calculates how much it thinks a family should be able to pay based on information from the Fafsa (and CSS) and the estimated annual cost of attendance. Financial need is the gap between the two. The school then determines how much in need-based aid (grants, workstudy and loans) the student is eligible for, and also applies non-need-based scholarships and other loan options to the equation. Parental finances aren’t considered for many graduate students.

- Accept the loan. Schools provide step-by-step details on how to transfer the funds from the federal government to their coffers. Some require borrowers to enter manually the dollar amount they want to borrow, while others automatically show the maximum amount allowed—and borrowers must take an extra step to borrow less.

- Complete mandatory online entrance counseling on the Federal Student Aid website acknowledging the rights and responsibilities of borrowers. It’s short and only required of student borrowers new to that particular loan type. Parents aren’t required to do it.

- Sign a document agreeing to the loan terms, known as a master promissory note. (That agreement is just for new borrowers; returning borrowers instead sign an annual loan acknowledgement.)

- Voilà! The school applies some portion of the loan to cover what it charges; additional funds borrowed for living expenses and other indirect costs will be paid directly to the borrower.

Direct PLUS Loan for Parents

For parents of dependent students enrolled at least half time (6-8 credit hours):

- Loan amount is maximum cost of attendance, less any other financial aid

- Parent is responsible

- Dept. of Education is the lender

Private/Alternative Loan

More expensive than Federal student loans

- Eligibility, interest rate and fees based on credit scores

- More information on private/alternative loans at www.finaid.org/loans/